Market Access Advisory: Regulatory & Legislative Intelligence

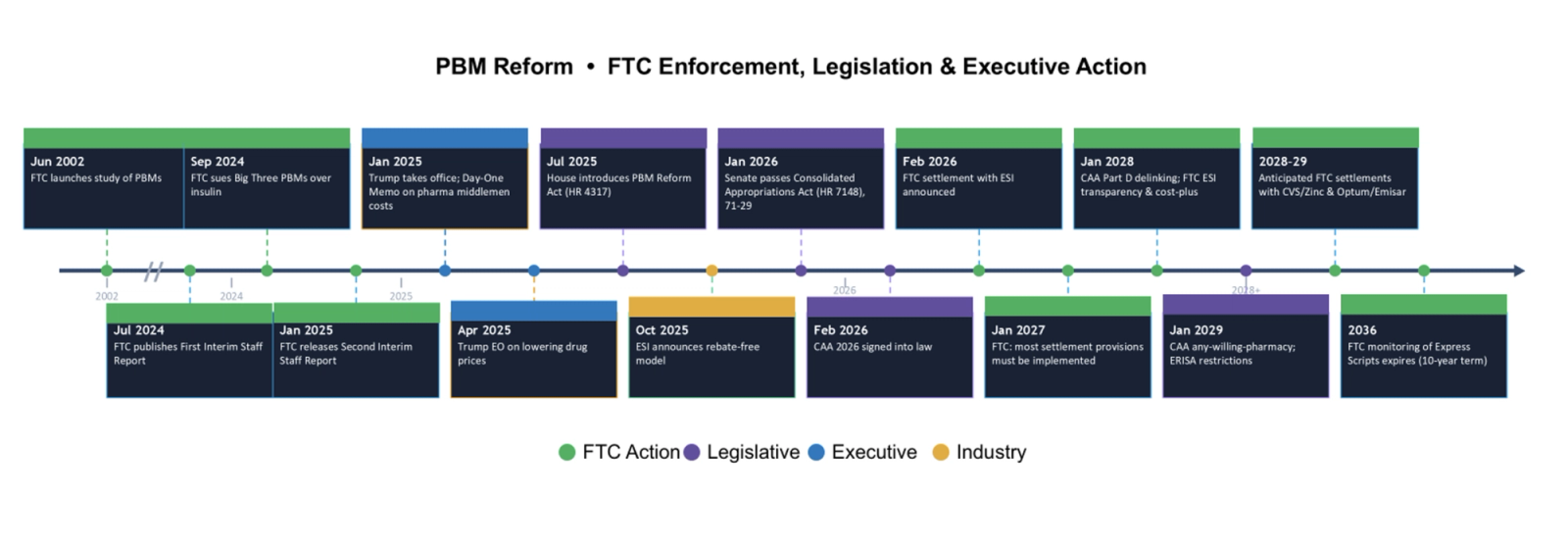

Much has happened this year, and it’s only early March. Years of scrutiny, public stakeholder pressure, and debate have pushed the issue of pharmacy benefit manager (“PBM”) practices past a tipping point – triggering a new era of regulation and legislative action.

This market access advisory examines how these changes are reshaping pharma market access strategy across pricing, reimbursement, and commercialization. The timeline below summarizes key events that have led to where we stand today:

Executive Summary

Over the past few years, biopharma manufacturers have been at the center of major policy efforts—from the Inflation Reduction Act to various Most‑Favored‑Nation pricing proposals—each aimed at reshaping how drugs are priced and paid for. Now, the same level of scrutiny is turning toward PBMs and their role as the middlemen in the pharmaceutical supply chain. Political focus on drug costs, often focused on headline list prices rather than actual net prices, has added fuel to the fire and pushed PBM practices into sharper view.

From a market access advisory perspective, these changes have direct implications for how manufacturers approach contracting, pricing, and gross-to-net management.

This pressure has helped accelerate a wave of enforcement and rulemaking: the Federal Trade Commission’s (“FTC”) settlement with Express Scripts, ongoing actions involving Caremark and OptumRx, new transparency and pass‑through requirements in the 2026 Consolidated Appropriations Act (“CAA”), and Centers for Medicare & Medicaid Services’ (“CMS”) tightened Bona Fide Service Fee standards within the 2026 Physician Fee Schedule Final Rule. Taken together, these are not isolated events—they signal a meaningful shift toward more visibility and accountability across drug pricing. Manufacturers will need to factor these changes into both corporate and brand strategy to stay ahead.

At the same time, the speed and visibility of this reform wave have created some misunderstandings about what PBM reform will actually deliver. Commentary often blurs the line between list‑price perception and net‑price reality, leading to sweeping assumptions that don’t fully match how the system works.

This article aims to cut through that noise, lay out critical next steps, highlight where the narrative is getting ahead of the mechanics, and clarify a few of the most common misconceptions surrounding PBM reform.

Below, we separate myths from operational reality across three dimensions critical to WAC strategy, PBM contracts, and gross-to-net forecasting.

Myth #1: PBMs Will No Longer Be Able to Favor High-WAC, High-Rebate Drugs

Reality: The FTC settlement doesn’t eliminate rebate‑driven formulary behavior. It applies only to a narrow set of dual‑WAC situations where the exact same molecule is sold at two different list prices—such as certain insulins and biosimilars. For example, Express Scripts (“ESI”) can’t prefer the higher‑WAC product unless its net cost is actually lower.

Outside of those limited scenarios, most drug classes operate with a single WAC, and PBMs still have broad flexibility to choose higher‑rebate products. Plan sponsors who prioritize rebate revenue to help manage premiums can continue to steer PBMs in that direction, and PBMs may continue to optimize around those incentives.

What’s really changing is that regulators are addressing a specific practice that has inflated patient out‑of‑pocket costs in dual‑WAC categories. But the fundamental economic model—high list prices paired with deep rebates in competitive classes—may remain intact. For most manufacturers, especially in single‑WAC categories, the pressure to maintain rebate competitiveness is essentially unchanged.

Pharma manufacturers should maintain a disciplined market access strategy approach when evaluating pricing and rebate strategies within evolving payer dynamics.

Myth #2: Recent Reforms Eliminate Rebate-Based Compensation Models

Reality: The recent reforms change how PBMs can be paid, but they don’t make rebate‑based models disappear overnight. The FTC’s settlement with ESI requires that its standard offerings move away from compensation tied to list price and eventually support point‑of‑sale rebate pass‑through and the removal of guaranteed rebate amounts. But the settlement also includes a “meets competition” provision, allowing plan sponsors—if they request it in writing—to keep legacy benefit designs that mirror today’s high‑WAC, high‑rebate structures. In other words, the reform nudges the market toward delinking drug price and PBM payment, but it doesn’t force every plan sponsor to change immediately.

The CAA reinforces this shift, but it does so differently across markets. In Medicare Part D, PBMs can continue negotiating rebates, but they can’t keep any of the value as compensation—only flat, bona fide service fees qualify. In the commercial market, the law takes an indirect route by making the plan sponsor the beneficiary of all price‑linked value and leaning on Employee Retirement Income Security Act of 1974 (“ERISA”) fiduciary rules and new transparency requirements to reshape PBM incentives over time.

The net effect: rebate‑linked economics are beginning to unwind, but not abruptly. As long as some plan sponsors still request benefit designs built around traditional rebate guarantees, PBMs will continue operating in both old and new models during the transition. The full market shift will take time; However, manufacturers should be strategizing around these shifts now.

This underscores the importance of a proactive market access advisory approach as manufacturers reassess pricing models, contract structures, and rebate strategies in a transitioning landscape.

Myth #3: Rebate Pass-Through Requirements Will Be a Game Changer

Reality: The CAA mandates 100% rebate pass‑through to ERISA‑governed employer plans, but this largely reflects what many big employers already have in place. Studies show that most large self‑funded employers already receive nearly all of the rebates negotiated on their behalf, and national accounts frequently push pass‑through rates above 90%.

In practice, many sophisticated employers have already moved toward full or near‑full pass‑through because of fiduciary expectations and pressure from their consultants. The CAA essentially takes what has become common among these larger buyers and turns it into a baseline requirement for all ERISA plans—full pass‑through, quarterly remittance, and audit rights. While the statutory effective date is January 1, 2029, the shift will start showing up much earlier as contracts come up for renewal.

Myth #4: Cost + Plus Approach Will Save Pharmacies

Reality: Moving to a cost‑plus reimbursement model may improve transparency, but it doesn’t guarantee pharmacies will be financially sustainable. Pharmacy trade groups have already signaled that a simple “cost + dispensing fee” structure won’t reliably cover operating costs—especially given how widely those costs vary across generics, brands, and specialty products.

On top of that, determining the actual “cost” of a drug isn’t as straightforward as it sounds. Benchmarks like National Average Drug Acquisition Cost (“NADAC”) fluctuate, acquisition prices differ across wholesalers and contracts, and pharmacies often lack real‑time visibility into what payers will recognize as the allowable “cost.” As a result, cost‑plus models can still leave pharmacies underwater on many fills.

In short, while cost‑plus frameworks may bring more clarity to how reimbursement is calculated, they don’t inherently ensure stable margins—or solve the broader financial pressures community pharmacies face today.

Even with the noise surrounding PBM reform, there’s no question this round of changes is meaningful. The FTC settlement, CAA pass‑through requirements, and new BFSF rules will force updates to long‑standing contracting practices and create real shifts in how value moves through the system.

At the same time, some of the early narratives have gotten a bit ahead of the facts. These reforms don’t rewrite every part of the model overnight, and the details matter. Manufacturers will need to look closely at the practical implications—how contracts need to change, how pricing and GTN models should adapt, and where risk may surface—rather than relying on broad assumptions.

It’s equally important to recognize that payers won’t sit still while these rules roll out. Many have been evolving their revenue strategies for years, and this reform cycle may only speed that up. As pricing‑linked compensation tightens, large payer‑PBM organizations are likely to lean even harder into vertical integration—expanding into provider groups, specialty clinics, and even hospital systems to maintain control over cost and margin. So while PBM reform may ultimately reshape the landscape, payers’ own strategic moves will shape it just as much, requiring a more disciplined market access approach as pharma manufacturers adapt pricing, GTN, and contracting strategies.

For manufacturers, success will come from balancing disciplined compliance with a clear view of where payer incentives and power dynamics are heading next.

What Manufacturers Should Do Now and How IntegriChain Can Help

- Develop an operational roadmap anchored to key FTC and CAA timelines: align compliance tasks, operational changes, strategic decisions, and financial planning.

- Validate government pricing treatment across all PBM / GPO agreements: confirm alignment with BFSF standards and assess implications for Average Manufacturer Price (“AMP”), Average Sales Price (“ASP”), Best Price, Medicaid rebates, and 340B.

- Stand up a rapid‑response process for evaluating new PBM contract structures: assess BFSF compliance, prepare fair market value documentation, and streamline legal/pricing/compliance review paths.

- Evaluate likely payer strategy shifts: model scenarios for reduced rebate influence, alternative fee structures, and potential coverage or formulary access changes.

- Prepare to review and redline overhauled payer contract terms: PBMs/GPOs are currently proposing contract and fee-restructuring which will go into effect January 1, 2027. Manufacturers should continue to anticipate new fee schedules, service definitions, reporting expectations, and audit rights, and should establish deal‑desk guardrails.

- Assess alternative fee structures and amounts and forecast changes against current fees.

- Review contract language for optimized contract operations and to enable appropriate disputes.

- Confirm that contract systems have capabilities and are set up appropriately to align with alternative contract structures.

- Ensure reporting systems and business analytics capabilities are updated to reflect alternative contract structures and information for decision support is captured.

- Assess cross‑benefit implications for pharmacy and medical products: evaluate impacts on specialty management, carve‑outs, rebate structures, and medical‑pharmacy integration.

- Update payer deal models to handle new contract structures: incorporate alternative service models, stress‑test utilization and access outcomes, and support real‑time negotiation scenarios.

- Modernize GTN decision‑support tools: integrate new payer contracting archetypes and assess financial implications across Medicaid, Medicare, 340B, AMP, and Best Price.

- Prepare for potential OPEX reclassification: determine how movement from percentage‑based fees to flat or activity-based fees affects accounting treatment and documentation requirements.

This pharmaceutical market access advisory is for informational purposes only and does not constitute legal, accounting, or regulatory advice. Manufacturers should consult qualified counsel before implementing changes based on these developments.

If you have any questions, please reach out to Consulting@IntegriChain.com or contact your Advisory lead.